OPERATIONS MANAGEMENT

CHECK POINT 74: OPERATIONS CONTROL

This Check Point Is Available By Subscription Only,

But You Can Still Check Out The Menu Below. |

|

| |

|

DO I NEED TO KNOW THIS CHECK POINT?

|

| |

OPERATIONS MANAGEMENT

CHECK POINT 74: OPERATIONS CONTROL

Please Select Any Topic In Check Point 74 Below And Click. |

|

| |

|

DO I NEED TO KNOW THIS CHECK POINT?

|

| |

WELCOME TO CHECK POINT 74 |

|

| |

HOW CAN YOU BENEFIT FROM CHECK POINT 74? |

| |

| The main purpose of this check point is to provide you and your management team with detailed information about Operations Control and how to apply this information to maximize your company's performance. |

| |

| In this check point you will learn: |

| |

• About operations control factors.

• About lean operational guidelines for operations control.

• About two main functions of operations control.

• About work dispatching activities.

• About work expediting activities.

• About four types of operations control systems.

• About steps in a job control and batch control manufacturing.

• About flow control and line balancing activities.

• How various operations control activities fit together within a company.

• About operations cost control system... and much more. |

| |

LEAN MANAGEMENT GUIDELINES FOR CHECK POINT 74 |

| |

| You and your management team should become familiar with the basic Lean Management principles, guidelines, and tools provided in this program and apply them appropriately to the content of this check point. |

| |

| You and your team should adhere to basic lean management guidelines on a continuous basis: |

| |

| • |

Treat your customers as the most important part of your business. |

| • |

Provide your customers with the best possible value of products and services. |

| • |

Meet your customers' requirements with a positive energy on a timely basis. |

| • |

Provide your customers with consistent and reliable after-sales service. |

| • |

Treat your customers, employees, suppliers, and business associates with genuine respect. |

| • |

Identify your company's operational weaknesses, non-value-added activities, and waste. |

| • |

Implement the process of continuous improvements on organization-wide basis. |

| • |

Eliminate or minimize your company's non-value-added activities and waste. |

| • |

Streamline your company's operational processes and maximize overall flow efficiency. |

| • |

Reduce your company's operational costs in all areas of business activities. |

| • |

Maximize the quality at the source of all operational processes and activities. |

| • |

Ensure regular evaluation of your employees' performance and required level of knowledge.

|

| • |

Implement fair compensation of your employees based on their overall performance.

|

| • |

Motivate your partners and employees to adhere to high ethical standards of behavior. |

| • |

Maximize safety for your customers, employees, suppliers, and business associates. |

| • |

Provide opportunities for a continuous professional growth of partners and employees. |

| • |

Pay attention to "how" positive results are achieved and constantly try to improve them. |

| • |

Cultivate long-term relationships with your customers, suppliers, employees, and business associates. |

|

|

|

1. THE PURPOSE OF OPERATIONS CONTROL |

|

|

THE PURPOSE OF OPERATIONS CONTROL |

Business owners and operations managers must be fully familiar with the basic elements and procedures of operations control which represents one of the most critical functions in every organization.

The main purposes of Operations Control are to authorize operational activities, to ensure effective implementation of operations planning efforts, and to control operations costs within the facility.

The effectiveness of operations control depends upon several factors outlined below. |

OPERATIONS CONTROL FACTORS |

1. |

Detailed preliminary planning of each job. |

2. |

Thorough preparation of drawings, tools, and materials for each job. |

3. |

Timely availability of operational capacity and human resources. |

4. |

Built-in flexibility in the master schedule requirements. |

5. |

Continuous coordination of shop-floor activities. |

6. |

Clear communication in the operations department. |

7. |

High quality of operational performance. |

|

Note:

- • The term "Operations Control" is used in the context of a non-manufacturing or industrial service environment, e.g. electro-plating plant, packaging plant, automated dry-cleaning plant. This term is also used in the context of merchandising operations, i.e. wholesaler or retailer, and project or contract management operations.

- • The term "Production Control" is used interchangeably with the term “Operations Planning” in the context of a manufacturing environment.

- • Additional information related to operations control of Service Operations and Project And Contract Management Operations is provided in detail in Tutorial 4.

- • All information presented in this check point is based on traditional Western-type management approach. Lean Management is briefly introduced below and discussed in detail in Tutorial 1.

|

| |

ADDITIONAL INFORMATION ONLINE |

|

|

|

2. LEAN OPERATIONAL GUIDELINES FOR OPERATIONS CONTROL |

|

|

LEAN OPERATIONAL GUIDELINES |

In order to maintain successful performance in a highly competitive manufacturing or non-manufacturing environment alike, it is essential to be fully familiar with the existing Lean Operational Guidelines related to operations planning and control. These guidelines have been summarized earlier and are repeated below. |

In order to accomplish this task, you and your management team must become familiar with Lean Management principles, methods, and guidelines contained in this program and apply them to plant layout. These guidelines have been developed by management experts in the Toyota Motor Corporation in Japan and contained in the Toyota Production System (TPS) . |

MAIN ELEMENTS OF THE TOYOTA PRODUCTION SYSTEM |

|

Some of the Lean Operational Guidelines, based on Toyota Production System, related to plant layout are summarized below. |

LEAN OPERATIONAL GUIDELINES FOR OPERATIONS CONTROL |

1. |

Minimize equipment requirements for manufacturing and operational processes. |

2. |

Balance and synchronize all activities related to manufacturing and operational processes. |

3. |

Optimize manufacturing and operational cycles. |

4. |

Ensure level-loading of plant and machines in the manufacturing facility. |

5. |

Maximize the flexibility within the manufacturing facility. |

6. |

Reduce machine set-up times and change-over times within the manufacturing facility. |

7. |

Maximize the use of low-cost automation for manufacturing and operational processes. |

8. |

Maximize the use of NC and CNC machines within the manufacturing facility. |

9. |

Eliminate machine-time and equipment waste in the manufacturing and operational processes. |

10. |

Eliminate labor-time and material waste in the manufacturing and operational processes. |

11. |

Maintain production planning based on shorter, but cost-effective production runs of smaller production lots. |

12. |

Maximize the use of U-Type machine cells for production planning purposes. |

13. |

Maximize the use of cross-trained operators for a broad range of manufacturing and operational processes. |

14. |

Minimize the production and operational lead times for product manufacturing. |

15. |

Identify and minimize all non-value adding operational activities, e.g. counting, checking, moving parts, preparing documents, packing, re-packing, and so on. |

|

Lean Management is discussed in detail in Tutorial 1. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

3. TWO MAIN FUNCTIONS OF OPERATIONS CONTROL |

|

|

TWO MAIN FUNCTIONS OF OPERATIONS CONTROL |

|

|

|

Dispatching Of Work |

|

Expediting Of Work |

| |

|

|

|

4. WORK DISPATCHING |

|

|

DISPATCHING OF WORK |

The first function of operations planning in a manufacturing environment is Dispatching Of Work, or Work Dispatching, in accordance with pre-planned manufacturing activities.

The main purpose of work dispatching is to authorize and initiate coordinated manufacturing activities by means of releasing orders and instructions.

Dispatching of work imposes several requirements outlined below. |

DISPATCHING OF WORK |

1. |

Materials are available and are transferred to relevant working stations. |

2. |

Production aids, such as tools, jigs, dies, or fixtures are available and issued to relevant working stations. |

3. |

Drawings, specifications, bills of materials, and parts lists are prepared and issued to relevant working stations. |

4. |

Job cards or reports are prepared for all manufacturing operations. |

5. |

Quality control inspection reports are prepared. |

6. |

All production aids and drawings are returned to their correct locations upon completion of the manufacturing process. |

|

|

|

5. WORK EXPEDITING |

|

|

EXPEDITING OF WORK |

The second function of operations control in a manufacturing environment is Expediting Of Work, or Work Expediting.

The main purpose of work expediting, or Progress Chasing, is to provide overall control of all manufacturing activities once production has been set in motion.

Expediting of work imposes several requirements outlined below. |

EXPEDITING OF WORK REQUIREMENTS |

1. |

Any details which have been overlooked or which do not proceed according to plan are rectified. |

2. |

Job cards or reports are completed with all the necessary data related to performance and cost control. |

3. |

The progress of work between various stations and sections is in accordance with the master production schedule. |

4. |

Quality control is maintained on a continuous level. |

|

|

|

6. FOUR TYPES OF OPERATIONS CONTROL SYSTEMS |

|

|

THE OPERATIONS CONTROL SYSTEM |

The Operations Control System depends upon the type of manufacturing method employed by the company. The operations control system may be classified into four types illustrated below. |

FOUR TYPES OF OPERATIONS CONTROL SYSTEM |

|

|

|

|

|

|

|

Job

Control |

|

Batch

Control |

|

Flow

Control |

|

Just-In-Time

Control |

This type of control exists in a job shop production environment.

|

|

This type of control exists in a batch production environment. |

|

This type of control exists in a flow production environment. |

|

This type of control exists in a

Just-In-Time

Manufacturing environment. |

|

|

|

|

7. JOB CONTROL |

|

|

JOB CONTROL |

The major characteristics of a Job Shop, or intermittent manufacturing operation, include diversity of products and operations, small volumes, and short production runs.

Manufacturing orders arrive from different sources in a relatively unpredictable manner and often at short notice. Many of these orders require the manufacturing of new products and the preparation of additional drawings and tools. Furthermore, the job shop operation is accompanied by a diversity of raw materials and complicated inventory control requirements.

Some of the basic features of Job Control are outlined below. |

BASIC FEATURES OF JOB CONTROL |

1. |

Each order must be planned and controlled on an individual basis. |

2. |

A new parts list and route sheet must be prepared for every non-repetitive order. |

3. |

Special raw materials must be purchased for every new order. |

4. |

Operational capacity and labor resources can be planned only on a short notice basis. |

|

All basic steps related to job control are summarized below. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

8. BATCH CONTROL |

|

|

BATCH CONTROL |

Control of manufacturing activities in a Batch Production environment, or Batch Control, is quite similar to the job control procedure. Manufacturing orders arrive from various customers and are grouped into Batches of similar products.

Since many manufacturing orders are received on a repetitive basis, various components and products are manufactured and kept in stock. Thus, the economical level of work-in-process and finished goods inventory should be established and manufacturing activities planned and controlled accordingly.

Batch production usually entails manufacture of tens, hundreds, and thousands of the same items for delivery to customers over an extended period of time. Hence, it becomes easier to schedule and control manufacturing operations during a longer production cycle. The number of drawings and tooling and the diversity of raw materials are also reduced in the batch production environment.

Some of the basic features of batch control are outlined below. |

BASIC FEATURES OF BATCH CONTROL |

1. |

Most orders must be incorporated into batches of similar products. |

2. |

Each batch must be planned and controlled on an individual basis. |

3. |

A new parts list and route sheet must be prepared for every non-repetitive batch. |

4. |

Raw materials must be purchased in accordance with economic inventory level requirements. |

5. |

Operational capacity and labor resources can be planned one or more weeks in advance. |

|

All basic steps related to batch control are summarized below. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

9. STEPS IN JOB CONTROL AND BATCH CONTROL MANUFACTURING |

|

|

OPERATIONS PLANNING AND CONTROL |

All basic steps related to Operations Planning And Control in a manufacturing environment have been illustrated earlier and repeated below. |

JOB CONTROL AND BATCH CONTROL MANUFACTURING |

|

|

|

JOB SHOP PRODUCTION METHOD |

|

BATCH PRODUCTION METHOD |

| Step 1a: Receive customer's order and identify job requirements, i.e., specification, quantity, and delivery date. |

|

Step 1b: Receive customer's order and identify order requirements per product, i.e., specification quantity, and delivery date. |

|

|

|

| Step 2a: Enter the job into the Job Order Book, allocate a Job Number, and prepare a Job Card/s. |

|

Step 2b: Combine similar product requirements from various customers into one batch, enter relevant details into the Job Order Book, allocate a Batch Number, and prepare a Job Card/s. If the product is a stock item, consider minimum inventory level requirements. |

|

|

|

|

Step 3: Check availability of drawings, tooling, raw materials, bought-out components, operational capacity, labor, and sub-contracting services for each Job or Batch. Refer to Bill Of Materials and Parts List.

Step 4: Authorize preparation of drawings, withdrawal from stores or purchase of tooling, raw materials, components, and sub-contracting services. Confirm prices and delivery dates.

Step 5: Schedule each operation specified in the Route Sheet. Enter relevant details into the Master Production Schedule considering the expected availability of drawings, tools, raw materials, bought-out components, operational capacity, labor, and sub-contracting services.

Step 6: Load operational capacity and utilize labor in accordance with Master Production Schedule requirements when relevant drawings, tools, and raw materials become available.

Step 7: Dispatch drawings, tools, and raw materials to appropriate working stations and issue relevant job cards in accordance with the Master Production Schedule requirements.

Step 8: Expedite overall control of all manufacturing activities and ensure that work is progressing in accordance with the Master Production Schedule requirements. Always maintain strict quality control.

Step 9: Prepare the necessary components for final assembly and ensure that all finished goods are properly inspected prior to storing them in the finished goods stores or dispatching them to customers. |

|

|

10. FLOW CONTROL |

|

|

FLOW CONTROL |

Flow Control, or Manufacturing Control in a Flow Production environment is very different in comparison with job shop or batch production.

The prime characteristic of flow control is the continuity of the manufacturing process. The Flow Production Process is best described by a Conveyor Line, where a small range of standard products is manufactured in large quantities. High volume production ensures additional economies in the manufacturing process provided production facilities are adapted to the manufactured item.

Similar items are produced on a repetitive basis for stock, mainly, not for specific customer orders. All work stations are arranged to facilitate uniform and Continuous Production Flow. Optimally, the production line should be organized to allow the most effective use of the operational capacity and manpower resources on a regular basis.

When a production line is being used, the Detailed Routing Of Operations is incorporated in the manufacturing process.

The maximum production output available from each work station depends upon its capacity. Each station must be manned by an appropriate number of employees to facilitate smooth production flow. Some of the basic features of Flow Control are outlined below. |

BASIC FEATURES OF FLOW CONTROL |

1. |

All materials flow through work stations at a constant rate. |

2. |

The constant flow of materials demands that operational capacity and human resources can handle the given production volume. |

3. |

Production scheduling and control of individual operations must be synchronized with the overall production planning requirements. |

4. |

The repetitive nature of manufacturing operations simplifies the requirements for daily instructions and production reporting procedure. |

5. |

The availability of all materials, operational capacity, and human resources must be coordinated well in advance to ensure a smooth production flow. |

|

| |

LINE BALANCING |

Effective Operations Control necessitates that all stages of every manufacturing operation are properly balanced well in advance. It is advisable, therefore, to balance the workload at each station despite some time variation or idle time which may occur. This process is known as Line Balancing.

Line balancing entails selecting the most suitable combination of operations to be carried out at each Work Station in accordance with overall manufacturing requirements. It involves minimizing the number of operations, work stations, operational capacity, materials, and human resources required to attain a pre-determined production level. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

11. JUST-IN-TIME CONTROL |

|

|

JUST-IN-TIME CONTROL |

Business owners and operations managers should become familiar with the basic principles of Just-In-Time Control, which exists in a Lean Manufacturing Environment. This methodology may provide the manufacturing company with several important advantages, which could become very helpful in a highly competitive marketplace.

Since this type of environment is very different to traditional manufacturing methods, it is discussed in details separately in the context of Just-In-Time Methodology in Tutorial 4.

JIT Implementation is discussed in details in Tutorial 1. |

ADDITIONAL INFORMATION ONLINE |

|

|

|

12. SUMMARY OF ACTIVITIES IN OPERATIONS CONTROL |

|

|

OPERATIONS CONTROL |

Operations Control requires continuous coordination of activities in various departments within an organization as illustrated below. |

SUMMARY OF ACTIVITIES IN OPERATIONS CONTROL |

|

|

|

13. THE OPERATIONS COST CONTROL SYSTEM |

|

|

THE OPERATIONS COST CONTROL SYSTEM |

Another essential function of operations management is correlation of efforts with the financial department to facilitate thorough control of Manufacturing Costs and to ensure effective recovery of the company's expenditure.

This task is usually carried out by a suitable Operations Cost Control System. The main objective of an operations cost control system is to provide correct allocation of material, equipment, labor, and sub-contracting service costs to various manufacturing assignments and to secure the desired level of company profitability.

The control of manufacturing costs is frequently handled by a cost control clerk and is based on two costing methods. Both methods were discussed earlier as part of the Cost Estimating Procedures within the operations department and are repeated below. |

SUMMARY OF TWO BASIC COST CONTROL METHODS |

|

|

|

Job Order Costing |

|

Process Costing |

| Products and services are produced or supplied to special orders or in batches. |

|

Products and services are produced on a continuous "flow" basis. |

|

|

|

Service Company |

|

Service Company |

| Custom service is rendered to a special customer order on a non-repetitive basis. |

|

Standard service is rendered to several customers on a continuous "flow" basis. |

|

|

|

Merchandising Company |

|

Merchandising Company |

| Products are supplied on a wholesale or retail basis. |

|

Not applicable. |

|

|

|

Manufacturing Company |

|

Manufacturing Company |

| Products are manufactured in a job shop or batch production environments. |

|

Products are manufactured in a flow production environment. |

|

|

|

|

14. MAIN PARAMETERS OF OPERATIONS COST CONTROL |

|

|

The main parameters of the Operations Cost Control are outlined below. |

MAIN PARAMETERS OF THE OPERATIONS COST CONTROL |

1. |

Raw Materials And Bought-Out Components.

Used on a particular assignment. The cost of raw materials must be summarized to determine the total material cost contribution. |

2. |

Production Time.

Time spent on a particular assignment. The cost of production time must be determined by converting production time into an applicable hourly rate in order to calculate total labor and operational capacity cost contribution. |

3. |

Sub-Contracting Services.

Utilized on a particular assignment. The cost of sub-contracting services must be summarized to determine the total sub-contracting services cost contribution. |

|

| |

RECORDING OF MATERIAL COSTS |

Recording Of Material Costs is usually completed by using Material Requisitions prepared in advance for various jobs. The recording of production time, on the other hand, is carried out by means of Daily Time Sheets or Weekly Time Sheets summarizing the total number of hours spent on a particular job, or alternatively, by means of Job Cards prepared separately for various assignments. The recording of sub-contracting service costs is normally accomplished in a manner similar to the recording of material costs by using a Material Requisition. |

|

|

15. OPERATIONS COST WORKSHEET |

|

|

OPERATIONS COST WORKSHEET |

In order to determine the actual cost of a particular job, be it a product or a service, it is necessary to record all individual costs in the Operations Cost Worksheet.

All elements of the Operations Cost Worksheet are similar to the Cost Estimate Worksheet, with the only difference, that it includes the actual costs in addition to the estimated costs reflected in the Cost Estimate Worksheet, as illustrated earlier in Tutorial 4. This worksheet, in fact, can be used for dual purposes and can be helpful during cost estimating and cost control stages alike. This will also enable the operations manager to control actual time taken to complete each stage of the job and determine the actual profit or loss for each individual job in the operations department.

If the actual costs exceed the estimated costs, the client will still expect to be charged the price, based on the estimated costs, and any additional costs should be absorbed by the company. Conversely, if the actual costs are below the estimated costs, this could be kept by the company as an additional profit or passed on as an additional discount to client. More details related to Production Cost Control in a manufacturing environment are discussed next. |

|

|

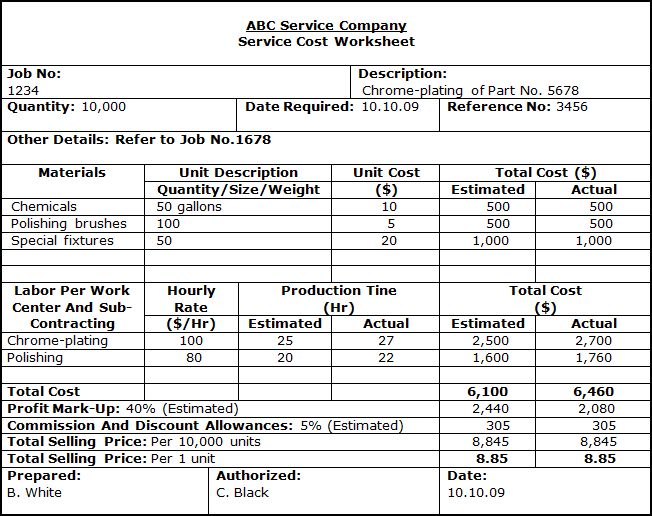

16. SMALL BUSINESS EXAMPLE

SERVICE COST WORKSHEET |

|

|

SERVICE COST WORKSHEET |

|

|

|

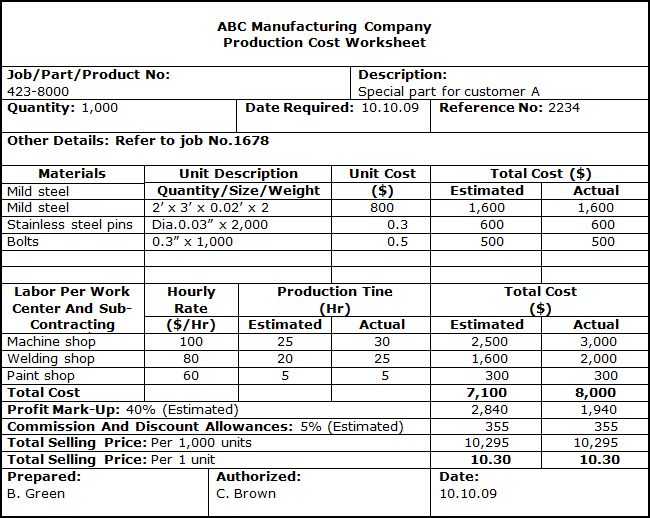

17. SMALL BUSINESS EXAMPLE

PRODUCTION COST WORKSHEET |

|

|

PRODUCTION COST WORKSHEET |

|

|

|

18. PRODUCTION COST VARIANCE |

|

|

PRODUCTION COST CONTROL |

The prime function of production cost control entails not only to accurately summarize all relevant Manufacturing Costs incurred in a specific manufacturing process, but also to compare actual production costs with the corresponding estimated production costs to ascertain that there is no negative variance, i.e. that actual costs did not exceed the estimated costs.

If as a result of the cost comparison it will be found that there is a positive variance, that means that actual production costs are actually below the corresponding estimated values, thereby providing a reassurance that the operations department is doing something right!

Irrespective, whether the Production Cost Variance is positive or negative, it must be identified quickly and reasons for such variance must be investigated as illustrated below. |

PRODUCTION COST VARIANCE EVALUATION |

1. |

Negative Production Cost Variance.

In case of a negative production cost variance, it is essential to identify whether it occurred as a result of material, or labor, or machine, or sub-contracting cost under-estimation. Upon identifying the reason, the appropriate costs must be adjusted for the next cost estimate purposes. |

2. |

Positive Production Cost Variance.

In case of a positive production cost variance, it is important to identify whether it occurred as a result of similar cost variables, and adjust same accordingly to avoid over-pricing, which may ultimately reduce the company's competitiveness in the marketplace. Positive production cost variance may also occur as a result of increased productivity within the operations department. If this is the case, such an improvement should be identified and appropriate personnel rewarded for their additional effort to maintain high level of motivation within the operations department. |

|

|

|

19. FOR SERIOUS BUSINESS OWNERS ONLY |

|

|

ARE YOU SERIOUS ABOUT YOUR BUSINESS TODAY? |

Reprinted with permission. |

|

20. THE LATEST INFORMATION ONLINE |

|

|

| |

LESSON FOR TODAY:

You Can Observe A Lot Just By Watching!

Yogi Berra

|

Go To The Next Open Check Point In This Promotion Program Online. |

| |

|